If you’ve spent any amount of time watching couples tour homes for sale on HGTV, you’ve probably heard the real estate agent talk about negotiating the closing costs with the seller. Those costs usually average 2-5% of the purchase price of your dream home. So, if your new home costs $200,000, expect to pay about $4,000 to $10,000 for these items. In a buyers’ market, you can definitely ask the seller to pay for these.

Before you make an offer on a home and negotiate a final contract with a seller, it’s a good idea to have a full understanding of what items are detailed in the closing costs. As we discussed in Part II of the Real Estate Due Diligence for Homebuyers series, title insurance is one of the three major types of insurance related to homebuying. This is one of the many items on the closing costs list.

Closing cost items could include:

- Recording fees

- Mortgage origination fees

- Appraisal fees

- Credit reports

- Inspection and re-inspection fees

- Pest inspection

- One-year warranty

- Survey

- Closing attorney/settlement fee

- Title search

- Municipal lien search

- Association information

- Broker transaction fee

- Mortgage transfer and assumption charges

- Deed stamps

Who pays for what closing costs?

All items are negotiable as to whom will pay for what and different states have different customary expectations as to what is a buyer’s cost and what is a seller’s cost, but typically the seller will pay for the lender’s title insurance. It’s important to keep in mind that whoever foots the bill will be able to choose who they work with. If you as a buyer are dead set on using a specific title insurance agency, you may have to end up paying for it. Most title companies will bundle the lender’s policy with the homeowners’ policy to help you save money.

Each state or region has standardized contracts used by real estate agents. Your real estate agent will communicate with the seller/seller’s agent on your behalf. If the seller accepts the offer and terms of the contract, you will be under contract and one step closer to home ownership. This contract is then given to the title agent or real estate attorney to perform or coordinate the items listed.

A deposit is required

When a buyer makes an offer on a home, you will often be required to provide an earnest money deposit. This money will go toward your down payment unless certain contingencies aren’t satisfied that cause the contract to cancel.

Examples of closing contingencies

A specified period of time to review condominium or homeowner association documents – some new buyers make the mistake of closing on a home in an association before reading all the by-laws and upcoming assessments. If the seller is pressuring you to the closing table before you have ample time to review this, don’t rush through these important documents. Be sure the contract gives you enough time to review this information and that you have a real estate attorney or agent review your concerns and specific questions about the documents.

A satisfactory home inspection – if there are major issues that require repair, you can walk away from the deal or renegotiate the terms of the contract.

An appraisal under the offer price – a lender won’t provide financing above the appraisal of the home

Financing– if you can’t get a loan approved, your deposit will be returned

A title survey – if the property is found to have any improvements that are encroaching on your neighbor’s property or an easement, you will want the seller to address this. Sometimes a seller’s agent will offer to use the current survey for the sale, but it’s highly recommended to get a new survey to ensure there are no issues.

Want to learn how to read a survey? Check out our Guide!

If these contingencies are met and you still want to cancel the contract, you may be in breach. Some buyers will use a home inspection or document review to wiggle out of a contract, but it’s much better to sign a contract when you are certain you want and can afford the home. Otherwise, you will lose your deposit along with the money you spent on the appraisal, a home inspection, survey, or any other upfront costs.

Never sign a contract unless you understand ALL the terms and are ready to make the final purchase!

Congrats! You are now under contract, so what comes next?

- Know your effective date.

The effective date is the day the last party signed or initialed and delivered the contract. This is very important as it is the starting point to determine the time periods on the contract related to the contingencies of the offer. - Submit your earnest money deposit

to open an escrow account with the title company with the contract or within 3 days of the effective date. Do not provide a check or money directly to the seller, even if it’s for sale by owner (FSBO). The title or escrow company acts as a neutral third party to collect and hold the earnest money check, loan documents, and signed deed. - Start your loan application.

During the pre-approval, the lender only references your credit history via a credit report. Final loan qualification depends on verification of other items like your income, employment history, assets, credit record, the value and condition of the property, and the status of the title to the property.

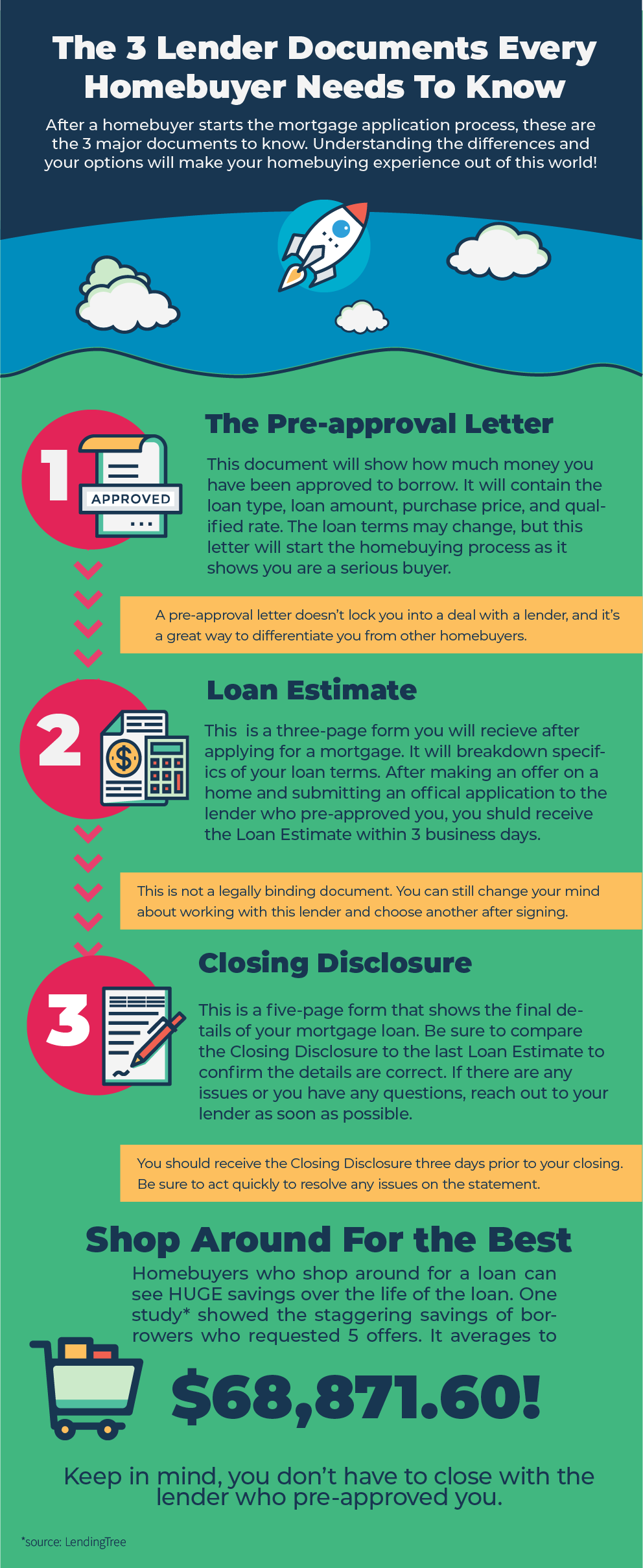

Three Lender Documents to Know: the Pre-approval Letter, Loan Estimate, & Closing Disclosure

There are three important lender documents to know when buying a home: the pre-approval letter, the loan estimate, and the closing disclosure.

The Pre-approval Letter

After you submit a mortgage application, you’ll receive the pre-approval letter from the lender. Keep in mind, it’s not unheard of for a consumer to receive an initial pre-approval and then later be denied a final loan at that interest rate, forcing the contract to cancel or accept a loan at a higher interest rate or lower loan amount. You should be especially aware of lenders who promise a loan approval in 24 hours. Typically, they are referring to the pre-approval. If a lender says you are approved for a loan, but you haven’t supplied any personal documentation to verify your assets, income, and/or employment, what they really mean is that you are pre-approved.

Pay attention to loan types, interest rates, terms, and prepayment penalties. Real estate industry experts are expecting mortgage rates to rise through the year.

Be realistic about what you can afford. Most financial advisors suggest that your total housing budget should not exceed 30% of your monthly income before taxes. As an owner, your monthly housing costs include your mortgage payments as well as home insurance, property taxes and condo or association fees.

If you are putting less than 20% down, expect to pay a private mortgage interest in your monthly costs and to put taxes and insurance premiums in escrow until the payment date when the amount is due. The reasoning for this is to protect the lender’s interest in the property. If the new owner doesn’t pay the taxes or assessments, a taxing authority could place a lien on the property, giving them higher priority than the lender’s lien. If a home is washed away in a flood or burned down, the lender’s protection goes with it if the insurance premiums aren’t paid.

The Loan Estimate

After you submit the mortgage application, the lender must provide you a loan estimate, also called a mortgage commitment letter, within three business days of receiving your application. This is the estimate of all costs, including estimated interest rate, monthly payment, costs of taxes and insurance, and how the interest rate and payments may change in the future. This form will tell you the amount of money you will need to provide at closing. The estimate will be high, so don’t panic! The lender has to cover some costs if underestimated. Review all the numbers and ask for explanations about ALL costs you don’t understand. This is not the final Closing Disclosure.

The Closing Disclosure

This is a five-page form that shows the final details of the mortgage loan. If you decide to move forward, the lender will ask you for additional financial information to finalize the loan terms. If any changes occur to an applicant’s finances, the lender may have the right to issue a new Closing Disclosure after the three day period according to new rules recently announced by the Consumer Financial Protection Bureau. As you move toward closing on a property, be aware of the loan estimate’s expiration date. Most expired within 30 days, but many lenders will work with you to extend the date if you are in the process of closing.

It should go without saying, but do NOT make any changes to your finances after you submit the application. Don’t fill out any credit card offers or go shopping for a new car during this time.

Getting down to brass tacks

Now that we’ve gotten the numbers out of the way, we’ll talk about the inspection period in part 4 and provide the buyer with a checklist of action items. Remember if you have any questions about the contract, to ask about it before signing. If you aren’t happy or comfortable with the terms of the contract, you should be ready to walk away. Buying a home can be an emotional experience for many, but it’s important to remember that this is also the biggest investment most people will ever make. Be sure to balance the emotional investment with the financial one.

Real Estate Due Diligence for Homebuyers: Closing Costs