This summer has seen record-breaking floods in areas with an unexpected and intense downpour of rain. While people brace for the worst in coastal areas of the Southeast during hurricane season, the months of flooding in the Midwest are far less common and causing severe damage to homes and businesses. It seems as though there is no end in sight in the fight against the Mississippi River flood.

These floods demonstrate just how important an elevation certificate and proper homeowners’ insurance is for homebuyers and businesses. While flooding like this would have been impossible to predict even a year ago, climate scientists say such extreme events will make reliable predictions even more difficult in certain areas.

If your home or business is in a high-risk flood area, an Elevation Certificate (EC) is required, but there are other key reasons to get an EC before purchasing real property.

What is an elevation certificate?

An elevation certificate is a document issued by the National Flood Insurance Program (NFIP) that shows important features of your property like its location, flood zone, building characteristics, and elevation of its lowest floor.

This certificate is used by homeowners’ insurance companies to determine your flood insurance premiums. There is a direct correlation between how high your property is above the Base Flood Elevation (BPE) and the cost of a flood policy. The EC of your property will be compared against the BPE. The lower the BPE, the higher your rate, and the higher the BPE, the lower your flood insurance costs will be.

Property owners who construct buildings at least three feet or more above the BPE will see significant savings on flood insurance premiums.

How much does an elevation certificate cost?

This certificate can cost hundreds or even thousands of dollars, depending on your area. For a standard lot and block home, where the lot size is under 10,000 square feet, it will cost around $350 in addition to the cost of a survey.

Is an elevation certificate a type of land survey?

No. An Elevation Certificate is not the same thing as a land survey. It can be completed by your state-licensed surveyor when you hire them to conduct a new land survey. Architects and engineers are also able to issue an elevation certificate. There may also be a copy of an EC on file with your community or municipality. Sometimes, your property’s flood zone can be found on the deed.

Reasons every homebuyer can benefit from an Elevation Certificate:

- According to the FEMA, water damage from floods is one of the most common and costly hazards in the U.S.

- An Elevation Certificate (EC) is required for properties located in high-risk areas in order to determine your insurance premiums.

- Nationwide, flooding is becoming more common and expected to get worse in many areas.

- FEMA maps are out of date, so an EC may help you better determine risks to your investment.

- An EC will give you a clear idea of potential damage from rising waters and how to plan better for future building or remodeling.

When is an Elevation Certificate needed?

Zones with the letters A or V on a Flood Insurance Rate Map (FIRM) are considered high-risk areas. ECs are required for issuing flood coverage in these areas.

ECs are not required or used for rating insurance premiums in moderate-to-low-risk areas like Zones X, B, and C, undetermined risk areas like Zone D or certain high-risk areas eligible for other subsidies like Zones AR and A99.

A new EC is required should any substantial changes be made to a building in a high-risk area. This includes any sort of improvements that change the footprint of the home. The new EC needs to accurately reflect the new building characteristics and Lowest Floor Elevation. Otherwise, as long as the structure information is up-to-date, a new homeowner’s insurance agent can use the EC of the previous property owner or use the one on file to rate the flood policy.

An Elevation Certificate is still helpful even when it’s not required

Even if your property isn’t in a high-risk area, an elevation certificate can provide some vital information regarding potential flood hazards.

As sea levels continue to rise and building code requirements change over time, flood risks and maps will be updated. Land that is currently out of high-risk flood zones may not always be. If you are remodeling or rebuilding, elevating to lower your flood risks will result in lowering your flood insurance rates and reduce the financial impact of the next flood.

An Elevation Certificate will designate:

– Location and Flood zone: These zones include such designations that use the letters A, V, B, C, X, or D. Each one denotes a level of high to low flood hazard.

– Building Characteristics: Any home features or improvements made on the land.

– Lowest Floor Elevation: This is the area most vulnerable to flooding. Depending on the type of home, this will usually include features like the basement or garage. A professional surveyor is required to properly assess the appropriate elevation based on FEMA guidelines.

At the very least, be sure to check the address on FEMA’s Flood Map and any revisions to the Map and Flood Insurance Study reports for your community for a more comprehensive understanding of flood risks to your area. Make sure you are aware of your flood zone and even if you aren’t required to carry flood insurance, consider adding it to your homeowner’s insurance policy anyway to be safe rather than sorry.

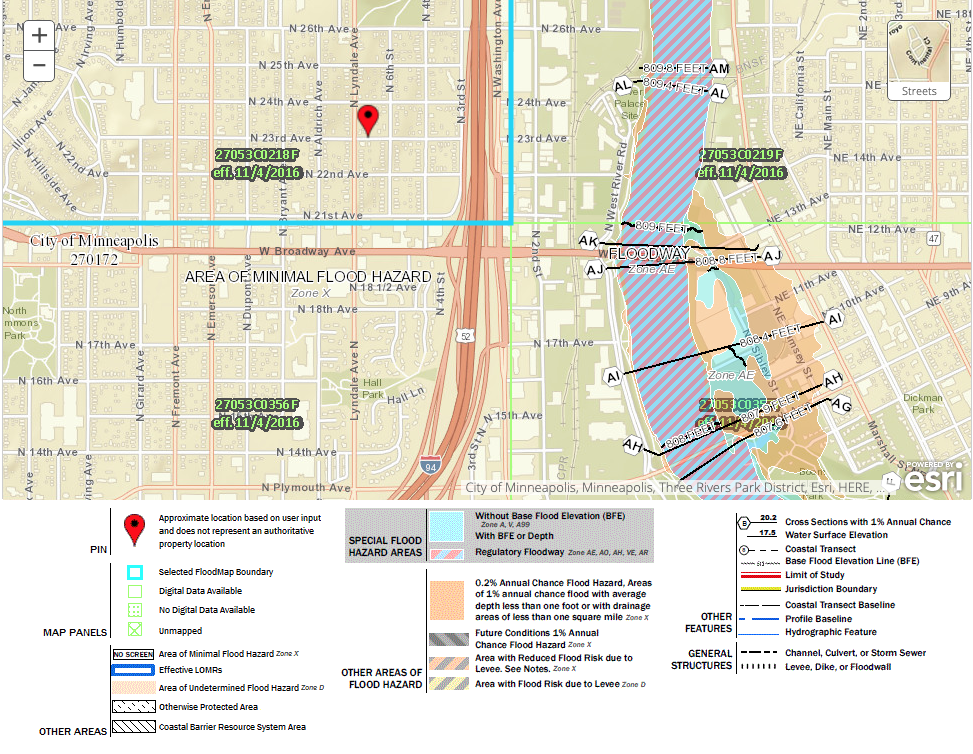

The City of Minnesota recently experienced flooding on I-94 and West Broadway Ave, which sits comfortably outside of the high-risk flood zone denoted below.

The proximity to the Special Flood Hazard Area meant that areas with minimal flood hazard experienced flooding.

Understanding the FEMA 100 year flood zone

You may have noticed on the image above there is an orange area designated as “Annual Chance Flood Hazard.” This is based on FEMA’s 100-year flood and 500-year flood maps, but these terms are somewhat misleading. Often, people assume this means that they will see flooding in this area within a 100 year or 500 year period. However, these are statistical averages that the orange area will see a 1% chance of flood in any given year, also “1-out-of-100” so the term “100-year flood” was adopted. When the statistical average of .2% is calculated for an area, the term “500-year flood” is used.

So, for a home in the 100-year flood zone, there is a chance your property may flood 1% of the time every year. If you are located in the 500-year flood zone, that likelihood is reduced to .2% in a year.

This does not mean that a flood will only happen in this area once every 100 or 500 years. It’s possible that mother nature may have other plans and flood this area twice in one year or not all. Natural disasters rarely follow the rules of probability to the letter. Instead of thinking of this as a fast and hard rule, it is simply meant to be a guideline for builders, homeowners, and community planners.

It’s dangerous for homeowners and homebuyers to assume that if they are out of a high-risk flood zone or even the 100-year flood zone area that they are safe from flooding. With enough rain, anything can and will flood.

The truth is that despite all our technological advances, predicting the weather still remains largely ineffectively — especially if we are trying to predict long term impacts. But one good rule of thumb to remember is that the closer you get to a flooding source, the more the “years” go down and the likelihood of flooding goes up. Your property may lie in the 50-year or 25-year flood plain, which can be found in FEMA’s Flood Insurance Study (FIS). Because there is so much data you won’t find these floodplain frequencies on the maps.

A better way to measure your home’s risk of flooding is to find the probability of it happening over the course of a 30-year mortgage depending on the flood zone.

- The 25-year flood zone means you have a 71% chance of flooding

- The 50-year flood zone means there is a 45% chance of flooding

- The 100-year flood zone means there is a 26% chance of flooding

- The 500-year flood zone means there is a 6% chance of flooding

Add flood insurance to your homeowner’s insurance policy

Approximately, 3% of the U.S. population lives in the 100-year flood zone. In theory, forcing people and businesses to relocate out of these areas could reduce insurance losses and protect people, but as everyone in real estate knows, land isn’t something we can build more of. Despite erosion and threats of flooding, coastal, river and lakefront living are still coveted commodities that are in high demand.

More than 20% of flood claims originate from outside of a flood zone. Floods are one of the most common natural disasters and only a small amount of water can do massive financial damage to a property. According to FEMA, one inch of water can result in $25,000 worth of damage. Homebuyers and homeowners want to make sure their investments are properly protected with a homeowner’s insurance policy that will cover flooding. Unfortunately, the basic policy doesn’t normally have flood insurance. So, when purchasing a home carefully consider the risks of a flood, understand that current FEMA map may not tell the whole story, and get flood coverage even if you aren’t required to carry it by your lender.