Lien Release Tracking for Real Estate Closings

Stay on top of lien releases without adding more work to your post-closing to-do list with Lien Release Tracking.

Avoid Title Clouds by Tracking Lien Releases

By utilizing a Lien Release Tracking service, you can move onto the next closing. When a release, satisfaction, or reconveyance hasn’t been filed on time, we start on resolution to ensure it gets done.

What’s included in our

Release Tracking Service

Lien

releases

Mortgage

satisfactions

Terminations

Subordinations

Reconveyances

About this integration

Closers' Choice

vendorsupport@closerschoice.comAbout Closers' Choice

Closers’ Choice continues as a leader providing closing software & title software to Closing & Title professionals for well over 35 years. Closers’ Choice, utilizing Closers Link, delivers Real-Time data to produce efficient settlements to Settlement Agents, Title Companies, and Real Property Law firms all across North America. Services Gateway is our new service that allows you to, with a simple push of a button, order your file’s requirements. No more logging in, no more passwords, and no re-key of your file’s data.

About this integration

E-Closing

support@e-closing.comAbout E-Closing

E-Closing is the title industry’s premier cloud based title production system. E-Closing is trusted by thousands of title professionals across the country. E-Closing is a powerful tool that can help modernize and streamline any title operation. Whether you are looking to provide better customer service, track business relationships, adopt a paperless environment or manage multiple offices, E-Closing equips title agents with the tools necessary to take their business to the next level.

About this integration

Qualia

vendorsupport@qualia.comAbout Qualia

Qualia is a one-stop shop for every aspect of a home closing, bringing consumers, lenders, title agents, realtors, and all other transaction participants together into one secure, mobile, cloud-based platform to increase compliance, close more transactions, and produce real-time connectivity for everyone.

About this integration

RamQuest

support@closingmarket.comAbout RamQuest

RamQuest is unwavering in our commitment to ensure a profound customer experience and continually strive to provide solutions that not just meet, but exceed expectations. But competing in business today is tough, and we know each of our customers also needs the experience we offer to stand with them, support them and back their business. RamQuest brings our entire team of title, technology and business experts to each and every customer engagement.

Six Sigma Quality Team

Dedicated Account Manager

Responsive Support

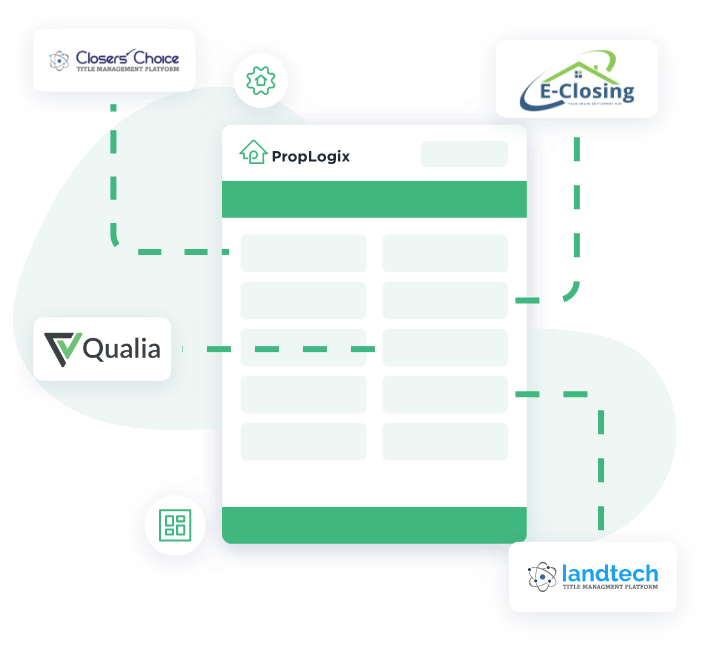

Title production help without leaving your closing software

Title production help without leaving your closing software

Connected to several leading title production softwares for ease-of-access to the services you need to get your work done.

See Our Integration Partners

Industry Partnerships & Designations

Inc. 5000 Honoree

PropLogix has been proudly ranked among Inc. Magazine’s 5000 fastest growing private companies for five years running.

ALTA Elite Provider

Each year since 2018 we’ve met the American Land Title Association’s strict standards to be named an Elite Provider.

FLTA Partner

As a Florida-based company, we’re committed to supporting the Florida Land Title Association as a vendor partner.

WFG Blocks Partner

As part of the WFG Blocks program, we’ve been vetted as a preferred title and settlement solution provider.

Starslink Partner

Since 2018 our due diligence services have been featured among Old Republic’s Starslink preferred vendor network.

Accuracy First

Each step of our research process has been designed by Six-Sigma Certified experts to reduce mistakes and ensure efficiency. Our Six-Sigma quality assurance team reviews each report before it gets to your hands so you can get to the closing table with confidence.

Timely Communication

Once the countdown to closing begins, every second is vital. When our researchers discover property issues, we tell you so you can get to work on resolving them. If you have a question, you can call or email and expect a quick response from our in-house support team.

Other Services That Save Title Professionals Time

HOA Documents/Estoppels

Alleviate association frustration and get estoppels or resale letters in time for closing.

Land Surveys

Get survey quotes from qualified surveyors fast and sit back while we take care of coordination for you.

Municipal Lien Search

Uncover municipal debt and issues before closing to ensure the homebuyer is protected.

Tax Certificates

Whether for a refinance or resale transaction, get a full picture of property taxes for your closing.

Payoff Letters

Save time by using PropLogix to request lender payoff letters so you can focus on your customer.

Title Curative

Our curative experts can help you find that missing link to get your closing back on track.

Title Reports

One-owner, two-owner, and full Title Reports available from a team of expert examiners.