Updated: July 27, 2021

The 21st-century real estate closing is radically different from closings of the past. Since 2011, there has been major acceleration for eClosings or digital closings, and laws and technology that allow eNotary or remote notary processes are the fuel. While I’m sure many of us are still wondering where those flying cars and hoverboards a la Back to the Future II are (hey, at least Nike made good on the self-lacing basketball shoes), closings of today are becoming easier and faster to complete.

As more states enact RON laws, more consumers will demand the convenience of remote notarization.

Here are the latest states that have approved the process, the model legislation that serves as the framework for many states, and some safety and implementation concerns to consider before you jump in.

What is Remote Online Notarization?

Remote Online Notarization (RON) allows banks, title companies, law firms, and other businesses to complete important transactions that require signatures and a notary seal remotely with the aid of online audio and video technology.

For settlement agents, this means that closing on a property doesn’t require all the parties to be in the same room. While notaries are required to be located in the state where they are commissioned as a RON, signers may be located anywhere with most RON laws.

Electronic Notarization vs. Remote Notarization

It’s important to distinguish between eNotarization and remote notarization. While they sound similar, there’s a key difference. The first allows documents to be signed and notarized digitally BUT requires the signer to be present in the same room as the notary. The latter takes that one step further and allows documents to be signed and notarized digitally and without the requirement of being in the same room, building, state, or, in some cases, the same country.

The Uniform Electronic Transactions Act (UETA) made it possible to use electronic signatures and storage of financial documents in digital formats in place of a traditional wet signature on paper. This was the first step in making eClosing and eRecording a reality. Other state and federal laws, including the “full faith and credit” clause of the US Constitution, the federal ESIGN Act, and other state statutes, act as the legal structure supporting electronic notarization.

Altogether, these laws establish two key principles: 1. Notaries are authorized to electronically notarize documents with eSignatures completed in the presence of the notary (not remotely) 2. When performed in compliance with one state’s laws, a notarial act executed in that state will be recognized as valid in another state, even if those states have conflicting rules and regulations on the process.

These well-established laws allowing eNotarization paired with new RON legislation is the catalyst for fully digital closings.

Get an inside look at the RON platform built for title professionals! Sign up for a ProperSign Demo!

What state was the first to pass remote online notarization?

Virginia became the vanguard of the RON movement when Governor Bob McDonnell signed a bill into law in 2011 and implemented the process in 2012. This was the country’s first bill to allow commissioned Virginia electronic notaries to notarize documents online via audio-video technology. Virginia’s law was an integral part of establishing some of the key principles of RON like defining “personal appearance” for a remote closing, how to verify the signer’s identity and the location of parties, and best practices for digital record keeping to ensure the notary seal is valid and tamper-proof.

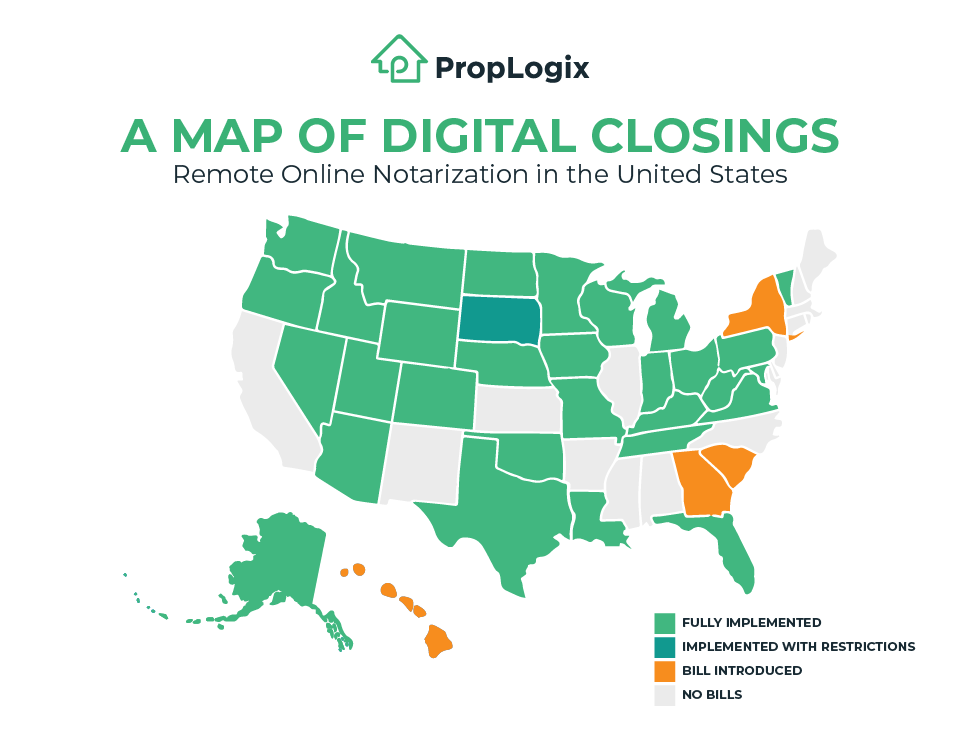

States that have passed Remote Online Notarization Acts so far

I wrote about how e-recording is changing real estate transactions in 2017, and at that time, only five states had passed remote notarization laws! Since 2011, 27 states have moved to pass Remote Online Notarization (RON), allowing for closing documents to be notarized without requiring all individuals to be physically present in the same room or even in the same state or country.

Here is the RON status of all 50 states:

Some states have issued emergency orders, proclamations, or bills to allow temporary use of audio-video technology to notarize documents remotely during the COVID-19 outbreak. These orders don’t necessarily meet the ALTA-MBA Model RON legislation’s standards and may not meet lender or underwriter requirements. “Fully Implemented” consists of permanent RON laws signed by governors, not executive or emergency orders.

Fully Implemented

- Alaska – SB241 was enacted on April 10th, and HB124 was enacted on April 30th, enabling remote online notarization.

- Arizona – Senate Bill 1030 went into effect on June 30th, 2020.

- Colorado – SB 20-096 went into effect on Dec. 31, 2020.

- Florida – went into effect on January 1st, 2020.

- Iowa – A RON bill was set to go into effect on July 1st, 2020. In light of the COVID-19 outbreak, an emergency declaration has suspended the requirement for a notary to be physically present immediately.

- Idaho – went into effect on January 1st, 2020.

- Indiana

- Kentucky – went into effect on January 1st, 2020.

- Louisiana – HB122 became effective on June 9, 2020.

- Maryland – Senate Bill 678 revises state notarial laws to allow remote online notarization effective October 1st, 2020. Order 20-03-30-04 waves the requirement of in-person notarization of documents during COVID-19. Notaries must affirm they are complying with the Maryland Secretary of State’s guidance and submit a Remote Notary Notification Form to remotenotary.sos@maryland.gov.

- Michigan

- Minnesota

- Missouri – On July 6th, HB 1655 was enacted, authorizing the use of remote online notarization with respect to acknowledgments and jurats. The Secretary of State will adopt standards and test and approve remote online notarization software before approved for use by a notary in the state.

- Montana – Governor Steve Bullock signed a law allowing remote online notarization in 2011, making Montana the second state to adopt RON after Virginia. However, it limited transactions to Montana residents. The law has been amended to allow remote notarizations for signers outside of the state starting on October 1st, 2019, but still requires the notary to be physically present in the state.

- Nebraska – An emergency rule allowed early adoption of Legislative Bill 186.

- Nevada

- North Dakota

- Ohio – went into effect on September 20th, 2019.

- Oklahoma – went into effect on January 1st, 2020.

- Oregon – Senate Bill 765 was signed into law by the Governor on June 15.

- Pennsylvania – effective on October 29th, 2020, the Department of State’s website has released Electronic and Remote Online Notarization guidelines.

- Tennessee

- Texas

- Utah

- Virginia

- Vermont

- Washington – Senate Bill 5641 went into effect on October 1st, 2020. The governor issued Emergency Proclamation 20-27 to allow the bill to take effect immediately during the COVID-19 pandemic.

- West Virginia – Senat Bill 469 was passed in March of 2021.

- Wisconsin – AB 293, based on the ALTA-MBA model, went into effect on May 1st, 2020. Wisconsin is the 23rd state to pass RON legislation.

- Wyoming – The Wyoming legislature passed SF0029 – Revised Uniform Law on Notarial Acts, allowing for remote online notarization and remote ink notarization in early 2020, and the governor signed it on February 9th. It went into effect on July 1st, 2021.

RON implemented with limitations

- South Dakota – HB 1272 allows for the use of video audio technology during a notarization only the notary “affixes the notarial officer’s signature to the original tangible documents executed by the [signer]” and only if the signer is personally known to the notary. This limitation is more akin to remote ink-signing notarizations (RIN), meaning that a fully digital closing isn’t possible in South Dakota. No bill to allow for a streamlined remote online notarization has been introduced.

Bill introduced

- Georgia – In February of 2021, HB 344 was introduced to “adopt certain standards for remote online notarization” and establish permanent use of RON. During COVID-19, an executive order suspends the requirement of physically appearing before the notary and “may be satisfied by the use of real-time audio-visual communication technology.”

- Hawaii – SB 2275 passed in both the senate and house. The bill was enrolled to the governor on July 13th, 2020, but hasn’t been signed yet.

- South Carolina – SB486 has been introduced to develop standards and requirements for remote online notaries, but no action has taken place since its introduction in 2019.

- New York – Before the governor signed Executive Order 202.7 allowing for emergency remote notarizations in response to COVID-19, Assembly Bill A4076B was introduced in 2019 authorizing electronic notarizations with the use of video and audio conference technology. New York Legislators passed Senate Bill S1780C in July 2021 and it awaits the governor’s signature.

No permanent RON bills

- Alabama – A supplemental state of emergency Proclamation allows notaries who are licensed attorneys or operating through licensed attorneys to use video-conference tools.

- Arkansas – Executive Order 20-12 suspends provisions requiring in-person witnessing and notarization of legal documents.

- California

- Connecticut – Temporarily allowing remote online notarization through executive order. Unless extended, modified, or terminated, it’s effective until June 23, 2020.

- Delaware

- Illinois – The governor signed an executive order temporarily approving RON as long as the notary and signer are in the state of Illinois at the time of notarization.

- Kansas

- Mississippi – HB 1156 does not authorize remote ink-signed notarizations or remote online notarization. Instead, it authorizes in-person electronic notarization (IPEN). The signer must appear before a notary in person to eSign and eNotarize the documents.

- New Hampshire – An executive order allows an individual and the notarial officer to ” communicate simultaneously by sight and sound through an electronic device or process at the time of notarization.”

- New Jersey – The Legislature passed Bill A3864 enabling remote online notarization, but the governor vetoed it on May 4, 2020. Executive Order 103 of 2020 and Bill A3903 allow for the emergency use of RON during the COVID-19 pandemic. The Division of Revenue and Enterprise Services released this guidance for notaries.

- New Mexico – Executive Order 2020-15 directs the Notary Compliance and Enforcement Unit to not recommend any discipline for any notary act involving audio-video technology and the notarization of a legible copy of a signed document delivered by either fax or electronic means.

- North Carolina

- Maine

- Massachusetts – Remote ink notarizations were approved during COVID-19 via S.2645. Read more details here.

- Rhode Island

The MBA-ALTA Partnership behind the legislative push for RON

A lot of progress has been made thanks to the collaboration between the Mortgage Bankers Association and the American Land Title Association to develop model legislation, creating a framework for remote online notarization implementation in any state. Since 2018, ALTA and MBA have been consulting with their member companies and state officials to create a law suitable to a multi-state environment. Based on a refinement of the 2017 Texas statute, the model law, if passed, endows a remote online notarization the same legal status as a notary executed in person.

An organization like the MBA, ALTA, and government entities have been working toward greater standardization for collecting, categorizing, and storing data required for a real estate closing. Every transaction requires accurate and legible data for a successful closing. The Uniform Closing Dataset regulation is another example of this push toward more streamlined data that serves as the backbone of the closing experience for professionals and consumers alike.

From the signing of the purchase agreement to closing day, this model legislation, if adopted by your state, is intended to enable the creation of a fully electronic mortgage experience by MBA and ALTA member companies who choose to go digital.

Some highlights from the MBA-ALTA model legislation:

- Robust provisions with multilayers of identity verification include a requirement for presentation of photo ID, credential analysis, identity proofing, and a digital recording of an audio/video communication capturing the notarization of documents.

- An easy way to distinguish between acknowledgments performed online and in person.

- No competitive advantages to any company by requiring specific technology in the bill, so there’s an even playing field between eClosing and RON providers.

- Technology requirements should also not be so restrictive that they hamper the evolution of technology and security improvement in the future.

- Secretaries of State are directed to use data standards developed by the Mortgage Industry Standards Maintenance Organization (MISMO) before final approval of regulations to implement the law.

- Conformity to the Uniform Electronic Transactions Act (UETA) and Uniform Real Property Electronic Recording Act (RULONA).

- Consumers are always given a choice in whether their closing uses remote online notarization or not.

This model legislation aims to create consistency among state RON laws and align government agencies with other organizations and private companies on the current and ongoing laws and best practices affecting real estate.

Now is the time to start preparing for a digital closing or at least a hybrid of some sort if you aren’t already performing them.

Is it safe?

Wire fraud is a huge concern of title agents and real estate attorneys everywhere. Business Email Compromise (BEC) and spoofing are common ways cybercriminals target consumers and settlement agents moving funds between parties. Technology is both a blessing and a curse. With the advent of new closing technology, real estate professionals need to understand how cybercriminals could dupe you and your clients.

There’s been a lot of buzz around deep fake videos lately, leaving many to question what’s real and what’s not. Sometimes used for entertainment like this video of a Steve Buscemi/Jennifer Lawerence mash-up, this technology creates a convincing scene. Steve’s visage moves fluidly over the expressions made by Jennifer’s face. Of course, the absurdity of this deep fake makes it easy to spot.

The nefarious implications of this technology being used to fake the identity of a contact in a real estate deal might send some chills down the spine of settlement agents.

Just when you’ve got your internal process down to combat wire fraud, payoff fraud, and other elaborate schemes of cybercriminals, now you might not even be able to trust your own eyes as you execute a remote closing over video.

I don’t say this to deter the use of remote online notarization. In fact, I think this is a necessary step in the evolution of real estate closings. But I think it’s important for early adopters to be cognizant of the potential threats. So far, there have been no news stories on deep fakes being used to commit wire fraud. Wire fraud is a threat in every closing present and future, even if you keep it old school.

The Future of RON Implementation

In addition to safety concerns, there are some key differences in state laws despite the efforts of ALTA and the MBA. Title agents will need to evaluate the logistical changes required within their internal process to be compliant with state-specific rules before allowing their notaries to perform RON closings.

Even if your state has passed RON legislation, the old way of doing things is still valid and may be preferred by some of your lenders and your underwriters.

To fully implement a digital closing, notaries and title agents will need to take note of:

- State requirements

- Lender requirements

- Underwriter requirements

Jason Somers of Fidelity explains more about this dynamic of “many masters” in the title industry.

A straightforward process like notarization becomes more challenging when done with new tools that have a risk of exposing sensitive data. In order to mitigate problems arising from fraud and cyberattacks, more stringent rules, regulations and costs are applied to the remote process. These new barriers and concerns may hamper the widespread use of remote online notarization for now.

However, for those who are willing to take the time to invest in the process, they may find a huge payoff in a market of global consumers who can’t make it to the closing table.

With the right precautions and continuing education, the future of real estate closings and remote online notarization looks bright.