Homeowners experience significant pressure to pay their property taxes, and local governments need homeowners to pay property taxes in order to fund local necessities like fire departments, schools, and law enforcement. As a result, tax lien and tax deed investing, also called property tax lending, exist to generate the lost revenue from unpaid taxes. This has become a big business since it started in Texas in the 1990s.

Tax lien certificates and deeds provide profit to investors willing to pay off the homeowner’s debt. While large institutions dominate this form of investing, anyone can choose to invest. Investors can profit by earning interest (and sometimes penalties) or potentially acquire below-market property.

Tax lien certificates are often confused with tax deeds and used interchangeably when there are major differences between the two. However, understanding how they work and the rewards and risks involved can ensure a profitable investment.

The Basics: Tax Liens, Tax Lien Certificates, and Tax Deeds

A property tax lien is one of many types of liens that may be placed on real property. Other types of liens include mortgage liens and mechanic’s liens. The lien discussed in this blog is a tax lien. Tax liens include real estate, personal property, and financial assets but tax lien certificates and tax deed investments are specific to real estate.

Despite sounding similar, a tax lien and a tax lien certificate are not the same. A tax lien is a claim a government makes on the property when taxes are delinquent. The tax lien certificate is a claim a purchaser has on the interest and fees made from overdue taxes.

A property tax lien is offered for public purchase as an investment in two forms:

- Tax lien certificate – bid for a collection of interest

- Tax deed – bid for ownership of property

Tax Lien Certificate

Different levels of government, from federal, state, and local, can place tax liens on a property, but tax lien certificates are offered at the local level (cities, towns, and counties). A Tax Lien Certificate is a bid on the right to collect interest on the delinquent property taxes, ranging from 2% to 36%, depending on the property’s location. The purchase of a Tax Lien Certificate entitles the purchaser to perform the duty of the taxing authority and collect full payment of the delinquent taxes. A tax lien is placed before a tax deed is sold. If the outstanding tax balance is resolved within the designated period set by the municipality, the investor is reimbursed their investment plus accrued interest and fees. If the debt isn’t paid, the property can go to a tax deed auction.

Tax Deed

Unlike a tax lien certificate, a tax deed entitles the purchaser to ownership of the property. Once a tax deed is sold at an auction, the property is transferred to the tax deed purchaser. Therefore, Tax Deed investors need to be more attentive to the property’s financial and physical condition as this form of investment is more deliberate.

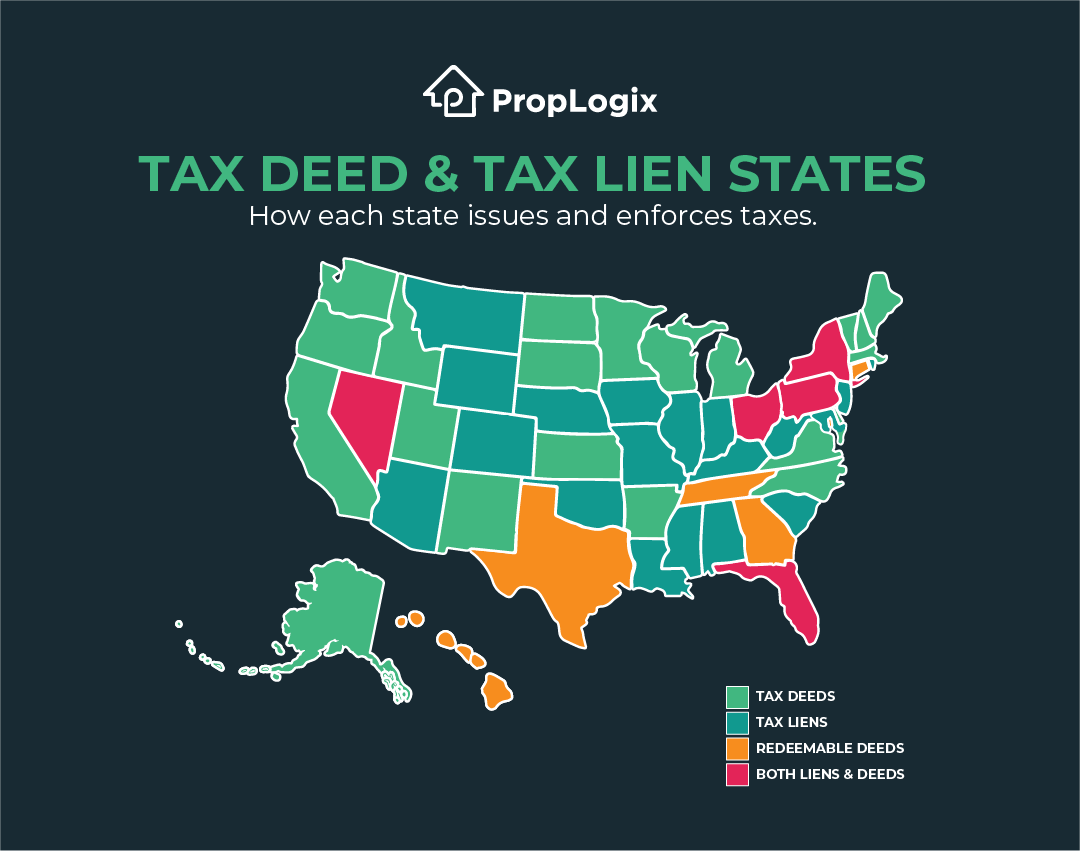

Tax Lien or Tax Deed State? Or Both?

Not all states offer both tax lien and tax deed sales. There’s also a third system to collect delinquent taxes call Redemption Deeds. Find your state below to find out which form(s) of property tax enforcement your state offers:

How Investors Leverage Tax Liens and Deeds

Unlike many forms of investing, tax lien and deed investments are immune to many of the fluctuations in the financial markets due to regulations from states rather than the federal government and generate a high-interest rate compared to other investments. Additionally, an investor can participate with relatively limited capital as liens can be purchased for as low as a few hundred dollars.

Every municipality has a different approach for auctioning off a tax deed or a tax lien certificate, but generally, there are 2 options:

- Live Auctions – This is the common method for smaller communities that don’t have online ca

- Online Auctions – As counties work to become more digitized, this is the most common option offered.

For Tax Lien Certificates, investors start with a base interest rate set by the municipality and bid down interest rates the investor is willing to accept.

For Tax Deeds, investors bid up from the opening bid (typically the amount of levied taxes, plus accumulated interest and penalties). A purchaser has the option to

- Foreclose on the property if the owner cannot pay off their taxes during the redemption period

- Pay off the debt, earning interest and penalties.

The county treasurer will post a list of properties that will be auctioned off several weeks before the auction. It is the investor’s responsibility to thoroughly research the property and potential risks of acquiring the tax lien certificate or the tax deed.

Investment Risks

Investing in a property based on its curb appeal is a common rookie mistake for investors. An investor may choose a property that they checked out via satellite view if the property is not local. This can be problematic if the satellite image is out of date. For example, a major storm could have recently caused a roof to collapse, but this may not appear on satellite view for another two years. Additionally, bidders have no legal right to enter the private property, so thorough research should not be taken lightly. According to the National Tax Lien Association (NTLA), investors should seek to avoid losses first and make profits second. Overall, a lack of property research can leave investors in a money pit. Other risks to consider include:

Municipal debt that may not be recorded as a lien yet

If a homeowner has neglected to pay property taxes, chances are, there may be other debts owed that could become a lien. This is commonly known as the “Gap Period.” Ordering a Municipal Lien Search or Tax Certificate can help uncover a potential lien not yet put in place.

Not to be confused with a tax lien or a tax lien certificate, a Tax Certificate is a comprehensive description of a property’s tax history and status. This document will show an unpaid balance with a taxing authority that collects separately and determine to whom a tax deed purchaser will be responsible for paying taxes in the future. This document is especially popular for properties in states like Texas, where taxes are often collected from separate authorities. For a thorough look into the tax status of a property, ordering a Tax Certificate can ensure a clean investment.

Municipal lien searches are more common in states like Florida. This report gathers information from various local departments like pending code violations, open or expired permits, unpaid utility bills, and more. Coupled with a search of property liens in the public record, a municipal lien search helps identify potential issues and improves risk analysis.

Consult a local real estate or title professional if you’re unsure about which report is most useful in your area.

Other liens found on the property

Mortgages and other liens will be wiped out upon sale, but certain governmental liens can survive a tax deed sale. Title reports or title searches are essential tools for investors to uncover any debts that may transfer with the title before the auction. Taking title via a tax deed sale reduces an investor’s ability to resell the property and acquire title insurance. It’s a good idea to connect with an investor-friendly title company or real estate law firm to help correct any title defects. In some cases, quiet title may be required to perfect the title.

Bankruptcy

If bankruptcy is declared on a property, a bankruptcy judge can order other debts to be paid off before the property tax lien, change the payment schedule, and even change the interest rate. Bankruptcy law varies by state but is important to factor into property research.

Tax lien certificates and tax deeds can offer a great return on investment, but hidden liens heighten the risks. However, with proper research and careful consideration of an investor’s end goal, investors can mitigate risks.

This content is provided for informational purposes only. PropLogix, LLC (PLX) is not a law firm; this content is not intended as legal advice and may not be relied upon as such. PLX makes no representations as to the accuracy, reliability, or completeness of this content. PLX may reference or incorporate information from third-party sources, upon which a citation or a website URL shall be provided for such source. PLX does not endorse any third party or its products or services. Any comments referencing or responding to this content may be removed in the sole discretion of PLX.