After setting a budget and deciding what type of mortgage is right, homebuyers will want to follow some of these tips to help the application process go as smoothly as possible. The pre-approval letter that you receive from a lender is not an official guarantee of a loan. Applying for a mortgage can be a long and difficult process to navigate, but understanding the options available to homebuyers will help!

The mortgage rate is not set in stone in the pre-approval letter, so be sure you are aware of what can influence changes and avoid the ones that you have control over at all costs (literally). Here are some things homebuyers should be aware of while shopping for a mortgage loan.

Three tips to get the best deal on your mortgage:

- Shop around for the best deal

- Don’t make any major financial changes while you are shopping for a house

- You can choose another lender if you don’t like the terms in the loan estimate

Want more real estate and title industry insights? Sign up to receive weekly updates!

When and where to apply for your mortgage

Get to know the lenders! Before you sign off on any loans, be sure to do your homebuyer’s homework (or due diligence) on the lenders. Some steps you should take to decide if a lender is right for you include:

- Check their consumer ratings

- Find out how many mortgage applications they approve and deny

- Try to get at least 5 offers from different lenders in order to comparison shop

If the lender has a high rate of denying applications, it’s a bad sign. Those who are already on the cusp of meeting typical requirements for a conventional loan may find it difficult to obtain a mortgage from a lender with a lower approval rate.

Getting quotes and originating a loan is fast and easy today thanks to mobile apps that put options right at your fingers. But don’t be too quick to pull the trigger. This is a big decision, and every first-time homebuyer should take their time.

Ultimately, every homebuyer should shop around for the best mortgage rate and be sure they are comfortable with the loan amount. Stick to your budget and don’t be persuaded to take on a more expensive home and bigger loan than you can afford under the expectation that real estate will always appreciate. While that is likely to happen, having a smaller mortgage that is manageable during good economic times and bad is better than a large one you could lose in a foreclosure.

What do I do after submitting a mortgage application?

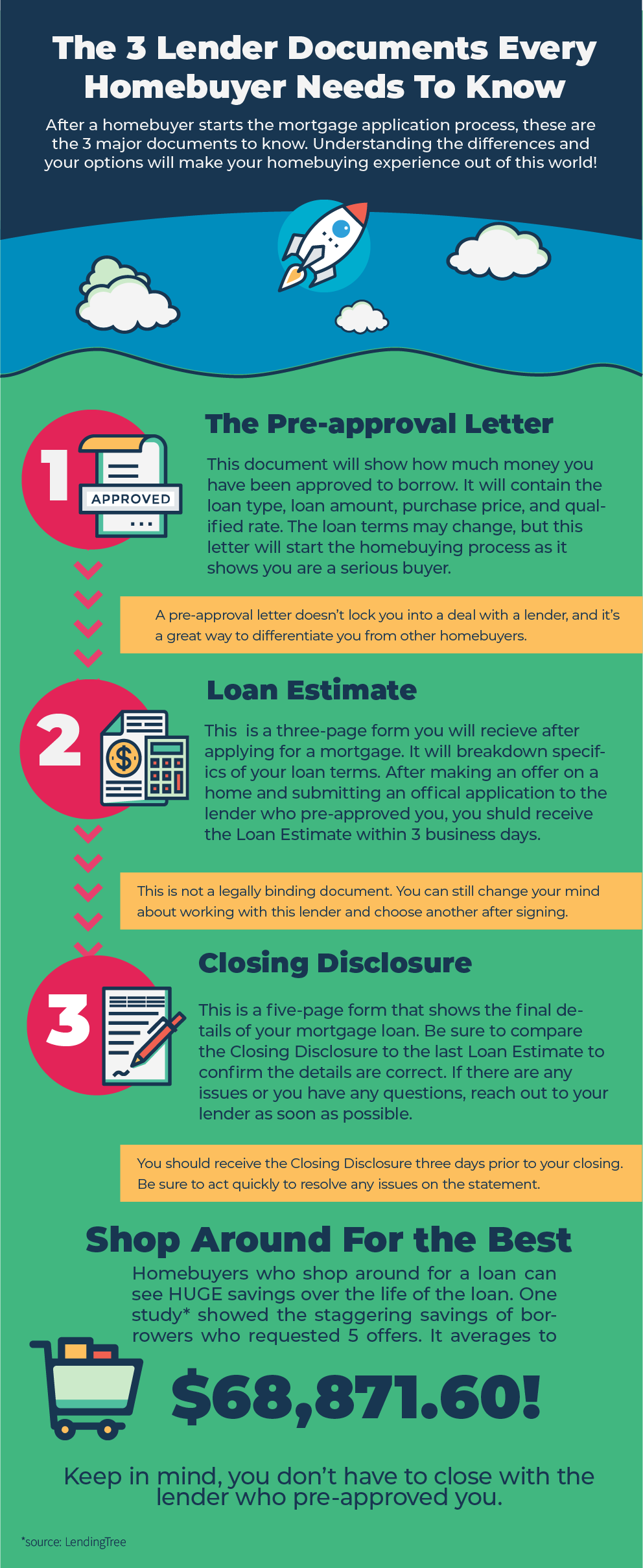

After submitting your application to the lender of your choice, you will receive a pre-approval letter. This will document exactly how much mortgage you have been approved to borrow.

Three important things to know about pre-approval letters:

- This piece of paper is a vital signal to realtors and sellers that you are a serious buyer.

- A pre-approval letter does not guarantee a home loan until you go through the underwriting process.

- The approval letter is time-sensitive.

Even though the loan terms may change, this is an integral part of starting the homebuying process. Only those who are ready to make an offer jump through this first hoop.

A pre-approval letter doesn’t lock you into a deal with a lender, but it’s a great way to differentiate you from other homebuyers. Other than the Pre-approval Letter, you should also get familiar with the Loan Estimate and the Closing Disclosure, which are important lender documents to help you track your closing costs. The infographic below explains how each one fits into the process of getting a mortgage.

What’s included in a pre-approval letter?

- Loan program

- Loan type

- Loan amount

- The purchase price

- The qualified interest rate

At this stage, you aren’t applying for an official loan yet. This is not a loan commitment and without a signature, this isn’t a legally binding document.

Until an Underwriter receives documentation to confirm your income and issues the Loan Estimate also known as the Mortgage Commitment Letter, there is a possibility the numbers in the pre-approval letter will change. This process doesn’t happen until after you make an official offer and send the pre-approval letter along with a Purchase Agreement Contract to the seller.

Every lender is different in the types of required documents for a mortgage pre-approval, but sometimes you may need to provide the following:

- Thirty days of pay stubs

- Two years of federal tax returns

- Sixty days or quarterly statement of all asset accounts including checking, savings, and any investment accounts

While in the pre-approval stage, be sure not to throw away any of these documents in case your first letter expires and you need an update. Even if the lender doesn’t require these documents at first and simply uses your credit report for the initial pre-approval letter, be sure to start saving these documents so you have them ready.

There should be no costs associated with the pre-approval letter until it goes to underwriting, and many banks will also waive the initial application fee.

Pre-approval letters are typically provided by lenders within 24 hours; however, the letter itself has a time limit. It’s usually only good for about 90 days, so be sure to check the letter for the expiration date. The letter will have two dates: when the letter was prepared and when the pre-approval expires.

A lot can happen within three months, and lenders need to have the most up-to-date information on your financial standing in order to give homebuyers a realistic idea of what they will be approved for.

Don’t worry though if you don’t find the right house in this time period, updating a pre-approval letter is usually a simple task. Your Loan Officer will request updated pay stubs, bank statements, and may run your credit again.

Limiting the impact of mortgage shopping on your credit

You don’t need perfect credit to get a pre-approval, but it’s important to be aware of how starting the pre-approval process will impact your credit history.

In order to get pre-approved, your credit must be pulled. This will count as a hard inquiry. Unlike a soft inquiry, a hard inquiry can ding your credit. Typically, if there is a hit, it’s just a handful of points, but several hard inquiries can be a bad sign for lenders.

Thankfully, credit bureaus have come to expect consumers to do some comparison shopping for the best rate.

While you are rate shopping among multiple mortgage lenders, keep the following in mind:

- Lenders must request permission from you before pulling your credit

- Mortgage applications are considered a hard inquiry

- Pre-approval isn’t binding — you don’t have to close with the lender that pre-approves you

- Lenders use a FICO scoring model that considers all inquiries within a specific time frame as one single hard credit pull.

Your time frame to shop before the inquiries start to add up could be anywhere from 14 to 45 days. Be sure to ask the lender which scoring model they use.

Additionally, FICO scores will ignore any hard mortgage inquiries in the 30 days prior to your scoring, so if you go to a second lender a week after getting pre-approved by the first, your first hard inquiry won’t be reflected in your scores yet.

This gives homebuyers a solid period of time to gather all the pre-approval information from multiple lenders to get the best deal.

8 things that can ruin your pre-approval with a lender

Your pre-approval is based on the information you give the lender at that time. If anything changes with your finances from then until the time you close on a house, you run the risk of your pre-approval terms changing or being outright denied a loan with that lender.

In order to avoid rejection during the closing process, be sure to NOT do the following:

- Apply for new credit

- Make a major purchase like a car

- Pay off all your debt

- Close a credit account

- Co-sign a loan

- Change jobs

- Fall behind on current bills

- Lose track of deposits — keep documentation of any and all activity in your bank account. It’s okay to take cash gifts from family or friends and put it toward your down payment, BUT you must be able to show where the money came from.

After pre-approval, you can keep an eye on your credit score using a free website like credit karma. Be sure to monitor it for any major swings.

Other things that may affect your pre-approval that are out of your control include:

- Loan requirements or lender guidelines change — it’s possible that they may raise the credit score, lower the debt to income ratio, or higher the required amount of savings for the borrower.

- Appraisal issues — depending on the type of loan you’re getting, there may be some restrictions on the condition and location on the property. You may have to choose another loan type option in order to close on that specific property.

After pre-approval, be sure to practice strict financial willpower, continue saving money in the event your closing costs are more than originally estimated, and start getting serious about finding and making an offer on a house that fits your budget.

Remember, if you go with one lender initially and later decide at closing that you would prefer another, you are not locked into that loan from the pre-approval.

This is a snapshot of a Loan Estimate. The signature is for confirmation of receipt, not a binding agreement to the terms. You can view a full example of a Loan Estimate at the CFPB website.

Keep your options for lenders open and don’t be afraid to find a better deal

If the terms of the loan estimate and subsequent Closing Disclosure don’t meet your expectations, you can change lenders before the closing. Those who shop around for a loan can see tremendous savings over the life of the loan. A chart from LendingTree shows the staggering savings of a borrower who requests 5 offers could save up to $68,871.60! It’s worth taking the time and effort to do it!

Remember, if your Closing Disclosure isn’t what you expected, be sure to ask your lender for clarification or correction before moving forward with the transaction. If the terms aren’t what you expected, you don’t have to close with that lender. Having those other offers available means you can reach out to another lender. To avoid a disruption in the closing, stay on top of all these documents and follow up with issues as quickly as possible.