Homeowners can use the equity they’ve accrued in their homes over the years to get more cash flow every month. There are two ways: Refinancing the terms and rate of your loan helps lower your mortgage or using your house as collateral to get cash when you need it.

An estimated 8 to 10 million homeowners could save on their monthly payments by refinancing. For those who may have tried in the past, lenders are being less picky in 2019. This means that even if a homeowner doesn’t have stellar credit or a higher debt-to-income ratio, there are still potential monthly savings available.

Here’s a breakdown of the refinancing programs available to homeowners, the benefits and drawbacks, and the role title agents play in the closing.

It’s important to first understand the differences in the refinance programs available and other ways that homeowners can use the equity in their home.

Different types of Refinance Programs

Traditional Refinance (also known as Rate and Term Refinance). A traditional refinance is when you replace your current loan for one with a better interest rate.

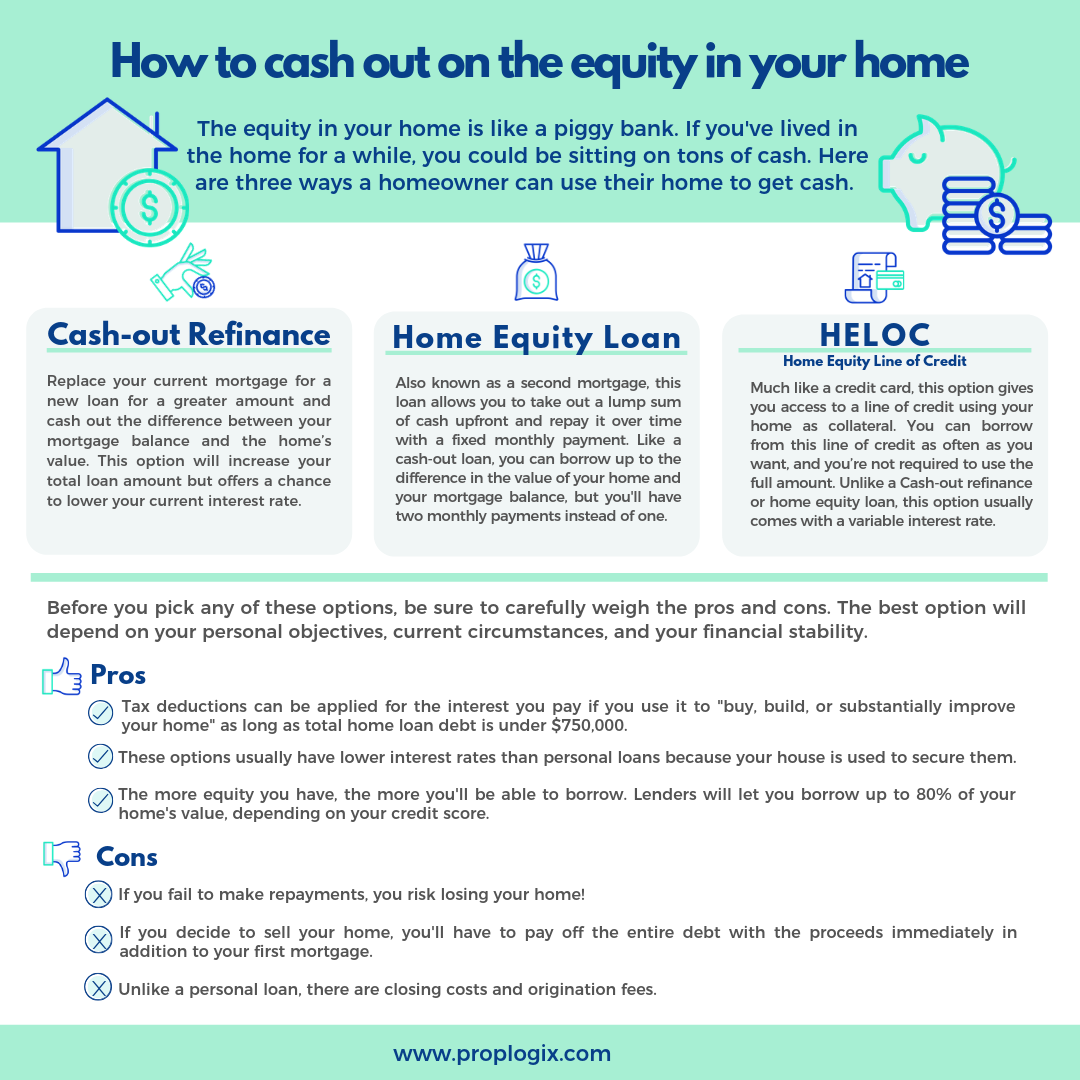

A cash-out refinance. Replace your current mortgage for a new loan for a greater amount and cash out the difference between your mortgage balance and the home’s value. This option will increase your total loan amount but offers a chance to lower your current interest rate.

Streamline Refinance. This is specifically for those with an FHA, VA, 203K or USDA loan. Those with a government-backed loan may qualify for a process that reuses the original loan’s paperwork, without a credit check or income verification. So, even those with bad credit might be able to take advantage of the current low rates!

Other Ways to Use the equity in your home to get cash:

Home Equity Loan. Also known as an equity loan or second mortgage, this type of loan allows homeowners to borrow money with their home as collateral. This loan allows you to take out a lump sum of cash upfront and repay it over time with a fixed monthly payment. Like a cash-out loan, you can borrow up to the difference in the value of your home and your mortgage balance.

Home Equity Line of Credit (HELOC). A line of credit, much like a credit card, using your home as collateral. Unlike a home equity loan, you don’t receive a lump sum but are approved for a maximum amount. You can borrow from this line of credit as often as you want, and you’re not required to use the full amount.

You’ll only pay interest on the amount you pull from your line of credit, which gives you more control over your total costs. Interest rates on HELOCs are variable. So, while it allows for more flexibility, there is a chance for volatility and unpredictability with this option.

Untapped equity is in many American homes

In less than a year, mortgage rates have fallen to rock bottom rates. In Mid-August of 2019, a loan that would have a quote of 4.94% in November of 2018 was priced at 3.6%. Even though these are both insanely low (In the early 80s, the United States witnessed the other end of the pendulum rate swing when mortgage interest rates on a 30-year fixed mortgage averaged 17%!), just a single percentage point can cost a homeowner thousands of dollars a year in interest.

In 2018, $56.5 billion of home equity was cashed out. That’s down from $92 billion the year before!

Even more astonishing is the estimates that total tappable equity available to homeowners during that time was $5.8 trillion.

Reasons to Refinance

There are lots of great reasons to refinance your home loan. Whether you should refinance or get a home equity loan or HELOC will depend on your objectives. Here are a few that might fit your specific circumstances:

- Save money over the lifetime of the loan. Lowering your interest rate means lower monthly payments and spending less money over time. If your current rate is higher than what is being offered to homebuyers, speak to several lenders to find out what sort of rate you could qualify for. Don’t speak to just one lender. Shop around to get the best rate. One study showed that borrowers who requested five offers for their first mortgage saved an average of $68,871.60 over the lifetime of the loan.

- Reduce your monthly payment. Lowering your interest rate will help to lower your monthly payments, but another way to make your monthly payments even lower is to extend the loan term, like from 15 years to 30. The problem here is that the longer it takes to pay off a loan, the more you will pay in interest in the long run. So, weigh your long-term objectives and short-term needs carefully. It may be more prudent to cut monthly expenses elsewhere… say one of those subscription services you forgot about?

- Pay off your mortgage faster. Another option during refinancing is to renegotiate the length of the loan. When you refinance from a 30-year mortgage to a 15-year loan, you’ll pay it off in half the time. You’ll pay less interest over time, but you’ll see higher monthly payments as a result. Additionally, you’ll also have less cash flow to put into other investments like your 401K or stocks. On the plus side, you’ll have more equity in the home to get a HELOC or home equity loan. If you have solid monthly earnings and your main objective is to be debt-free as soon as possible, refinancing to a 15-year loan is a good choice.

- Get rid of FHA mortgage insurance. Private Mortgage Insurance (PMI) and Mortgage Insurance Protection (MIP) are types of insurance homebuyers are required to purchase if they put less than 20% down at closing. PMI automatically cancels on conventional loans once the Loan-to-Value (LTV) reaches 80%. However, if your first loan was an FHA loan and you put down less than 10% at closing, the only way to terminate MIP is to sell the home or refinance into a conventional loan when you’ve accrued enough equity. Otherwise, you will be paying this monthly insurance premium for the lifetime of the loan.

- Fund your next renovation. Are you sick of looking at your kitchen cabinets? Want to build a deck in the back and host awesome parties? A cash-out refinance is a great way to get your next home improvement project done. A Home Equity Loan or HELOC are also two options for this objective. The repayment plan for each is different, so be sure to review the terms and conditions of each carefully to determine which is right for you.

- Switch an adjustable-rate mortgage for a fixed rate. The introductory rate period for an adjustable-rate mortgage is usually anywhere from 3-10 years, depending on your lender. If the time is almost up on your great introductory rate, now is a good time to switch to avoid an increase and establish a low and stable monthly payment.

- You want to consolidate your first and second mortgage. If you have a first mortgage and a variable rate HELOC or home equity loan, you may want to refinance to consolidate these into a single monthly payment. You may be able to convert a second mortgage with an adjustable-rate into one with a fixed rate and repay it with your first mortgage over a 15 or 30 year period.

- It’s all about the benjamins. Maybe you don’t want to spend the cash on something sensible like a home reno project that will increase the value of your home. Maybe you just want that cash money. Maybe you want to go on an extravagant cruise in the Mediterranean or you want to cruise the town in a Lamborghini. And why not?

A cash-out refinance, a HELOC, or a home equity loan can all help you achieve that dream. All of these options give you cold hard cash with no obligation to spend it on your home. While I can’t say that purchasing an asset without any return on investment is a good way to leverage the equity in your home, it’s your life, so live it how you want.

The Drawbacks of Refinancing

You have to do the math to determine if refinancing under your current circumstances and planned future is the right move. There’s no way around it. I don’t know how you feel about math, but I find it tedious and boring. BUT if there are huge savings to be had, it’s worth taking the time to break out your calculator and get some quotes from lenders.

Finding the right lender can be tough. Shop around for a lender with the best rates and makes you feel comfortable with the terms of the loan. Don’t feel pressured into getting a loan for more than you can comfortably afford. Getting quotes from multiple lenders will also keep your closing on track. If the first lender with the best quote falls through, you can quickly pivot to the next one and close on time.

It isn’t free. Remember those closing costs when you first bought the house? While there are certain items on the list that you won’t need to pay for again, but others, like the title search, will need to be ordered again to finalize your new loan.

You risk losing your home. While your interest rates are usually lower on a home equity loan than a personal loan, using your home as collateral means that the stakes are higher should you miss your repayments. If you are already struggling with your monthly payments, a cash-out refinance, HELOC, or home equity loan may not be right for you.

The Role of Title Companies in Refinances

According to our 2019 State of the Title Industry Report, 74% of title agents mostly handle resales, but refinances are still an important part of their job role. A new title search is always required by a lender to secure a first mortgage. This is also needed for a refinance. In addition to searching the public record and issuing a title policy that will protect the property rights of the lender and homeowner, the title agent also functions as the coordinator of the closing, ensures that funds are disbursed to the borrower, and provides any other post-closing services, like release tracking. They act as an intermediary between the property owner, attorneys, surveyors, lenders, lien holders, and government officials to resolve any title issues before refinancing.

When you first bought your home, you had your Realtor to help guide you through the process, but during the refinance process, you won’t have their professional advice to lean on. Since you are paying the closing costs during a refinance, the title company is your choice alone. As you would with choosing the right lender, take your time before you start the refinance process to review title companies and law firms in your area.