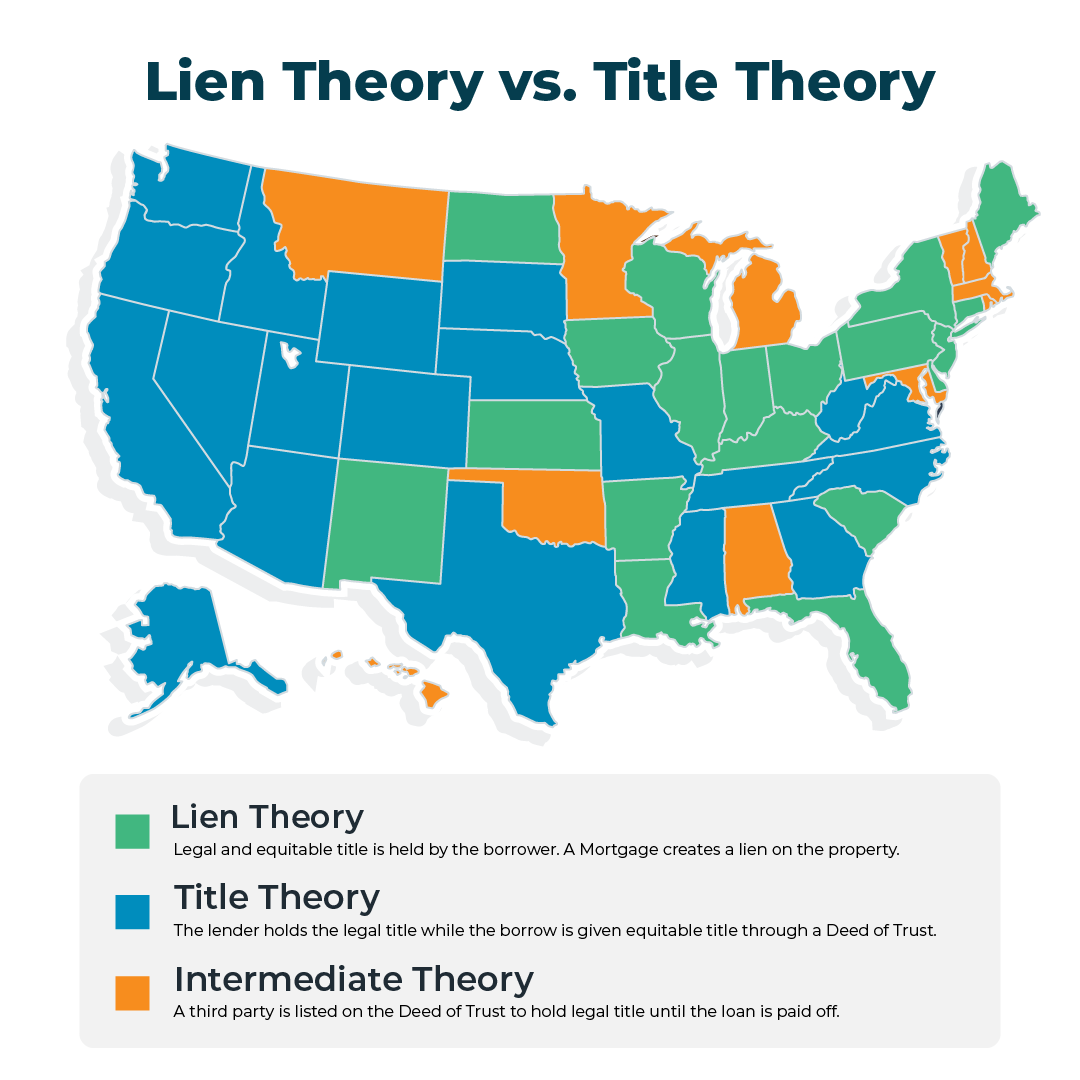

What is lien theory?

In lien theory states, the borrower holds the title to the property. Instead of a Deed of Trust, a Mortgage is recorded in the public record and acts as a lien against the property until the debt is paid off.

With a mortgage, a homeowner has both legal and equitable title. When the mortgage is paid in full, a release or mortgage satisfaction is filed in the public record to remove the lien.

Should a borrower default on a loan in a lien theory state, a judicial foreclosure is required for a lender to take possession of the property.

During the 2008 housing crisis, many borrowers in default used a “produce the note” defense in foreclosure proceedings that required lenders to demonstrate they had the legal right and authority to enforce it. The promissory note acts as an official IOU, so if the loan is sold off to another entity, both it and the Mortgage must be properly transferred.

While the defense is unlikely to be used successfully today and some states like Florida have addressed the issue with a law requiring the note at the time of the foreclosure, the process gives the homeowners a chance to defend their rights to the property and requires a lender to meticulously track and file the proper paperwork before initiating a foreclosure.

A judicial foreclosure usually begins with the filing of a Lis Pendens, which acts as a complaint against the borrower. The borrower is given a notice of complaint by either mail, direct service, or it’s published in newspapers, and he or she will have an opportunity to be heard in court. If the court finds that the debt is valid and in default, it will issue a judgment for the total amount owed, including court fees.

Like in title theory states, when a lender is found to have a valid complaint against a borrower, the house is auctioned off. Unlike title theory states, there is an additional step in which the highest bidder is subject to the court’s approval of the sale. Once that’s granted, the highest bidder becomes the new owner of the property.