We spend a lot of time giving tips to homebuyers, title agents, and Realtors to prepare for a real estate transaction, but we don’t talk as much about what to do after the buyers have signed on the dotted line. So we wanted to spend some time on what happens after homebuyers get their keys.

The new year brings the usual resolutions as well as a new tax season. Taxes are about as exciting as starting that new diet, but for homeowners, there are some important recent changes to their tax exemptions, deductions, and credits.

Homeowners should be aware of these things when filing their federal taxes this year.

Here are some key things to remember after you’ve received your keys:

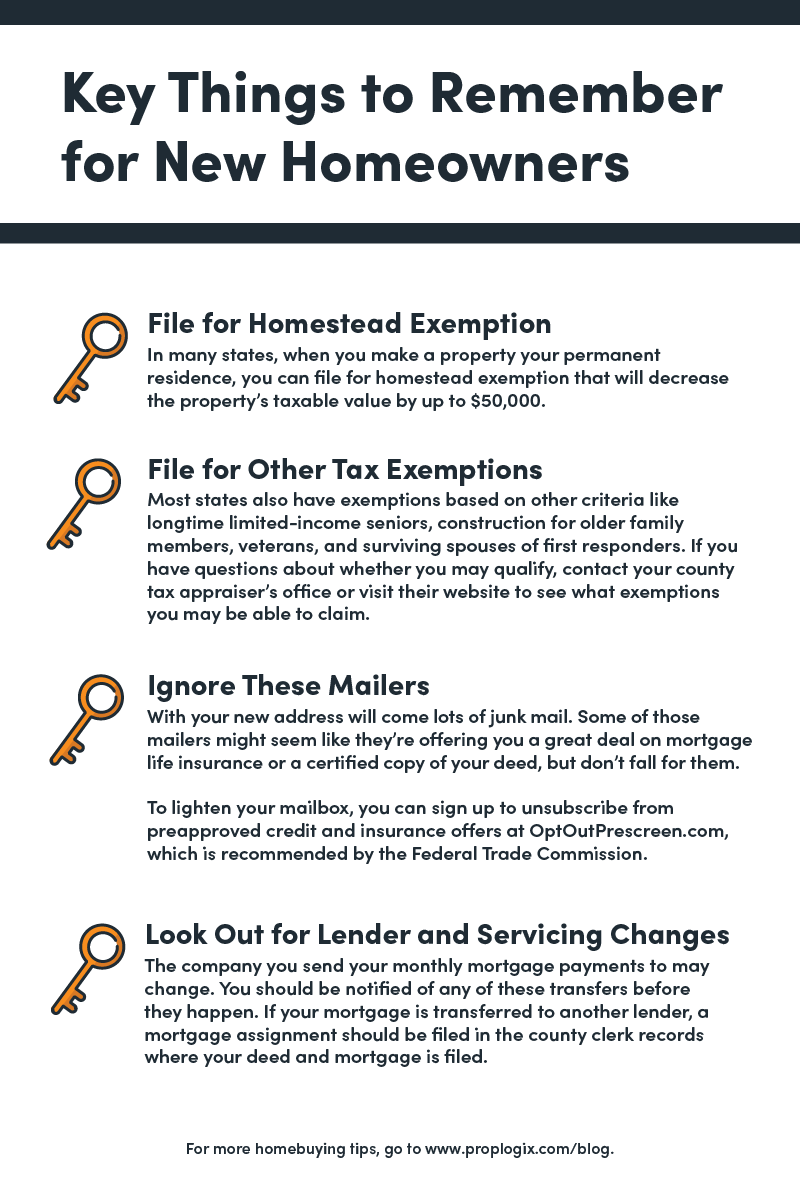

- File for homestead and other local tax exemptions that apply to you. In many states, especially Florida, when you make a property your permanent residence, you can file for a homestead exemption that will decrease the property’s taxable value by up to $50,000. Click here to learn more and download the Florida applications.

- Most states also have exemptions based on other criteria like longtime limited-income seniors, construction for older family members, veterans, and surviving spouses of first responders. If you have questions about whether you may qualify, contact your county tax appraiser’s office or visit their website to see what exemptions you may be able to claim.

- Ignore the scam mailers. You’ll get a lot of junk mail that may seem like they’re offering you a deal on mortgage life insurance or a certified copy of your deed. Don’t fall for them.

- Look out for Notices of Servicing Transfers. The company you send your monthly mortgage payments may change. You should be notified of any of these transfers before they happen. If your mortgage is transferred to another bank, a mortgage assignment is filed in the county clerk records where your deed and mortgage is filed.

Federal Tax tips for new homeowners

After some time, the reality (and sometimes hardships) of homeownership may damper that excitement you felt on the closing day. On top of the unexpected costs of fixing leaky sinks and replacing old windows with more energy-efficient ones, you have to worry about property taxes.

But there’s good news! As a homeowner, there are some tax benefits you can claim!

- Get Organized – Keep detailed records of your home-related expenses. Save all your receipts and organize them before tax season comes. You can go paperless by storing digital or scanned versions of your receipts on platforms like Dropbox or Google Drive.

- Learn about homeowner deductions – Deductions help to lower your overall tax burden by reducing your taxable income. As a homeowner, you may have enough eligible expenses to itemize your deductions.

- Determine if the standard deduction is better – If you decide to itemize your deductions, you forgo the standard deduction of $12,400 for individuals, $24,800 for married couples, and $18,650 for the head of households. The Tax Cuts and Jobs Act of 2017 limits the number of certain deductions, so you may come up short on tax benefits. In some cases, you might be better off taking the standard deduction.

- Save all your tax records – You never know when you might get audited. Save all your documents to back up your deductions. The law requires that you keep all the records you use to file your tax returns for three years from the date a return was filed. However, the IRS could go back as far as six years if there is a substantial error in a return.

Eligible home expenses to claim on Federal Taxes include:

- Mortgage Interest Deduction – Homeowners are eligible for this deduction on up to $750,000 of mortgage debt for your primary residence. If you have a home equity loan or HELOC that was used to make improvements on your home, that’s also eligible.

- Home office expenses – if you’re self-employed or use a room in your home solely for work purposes, you may be able to take certain types of deductions for expenses you incur for the home office and the depreciation for that portion of the home used.

- Energy-Efficient Updates – The IRS allows you to take a tax credit worth 30% of the cost of installing a solar energy system. Several states and local governments also offer property and sales tax exemptions when you switch to solar. The sooner you make this update, the better. The federal tax credit is set to expire after 2021.

- Home Improvements – other general home improvement expenses are deductible for the year you incur them, but when you sell your home in the future, it can lower your tax burden. Hold onto all your home improvement receipts so you can adjust the amount of capital gains taxes you’ll pay from the sale.

Owning a home can be expensive, but there are lots of benefits as well. Tax breaks can help shift the burden of homeownership to a more manageable load for many people. Follow these tips or reach out to a tax professional in your area to maximize these tax credits and deductions.

The Tax Cuts and Jobs Act impact on homeowners

In 2017, The Tax Cuts and Jobs Act was passed, creating one of the most sweeping changes to the tax code since 1986. While it provides small reductions to income tax rates for most individuals and significantly reduces the income tax rates for corporations, the act has rolled back or suspended previous beneficial tax deductions for homeowners.

The new act suspends or limits many of the itemized deductions that homeowners have used in the past to save money on their tax bill.

In the past, homeowners could deduct the interest paid on first and second mortgages up to $1,000,000. The new act caps that at $750,000 now.

The deduction for state and local taxes has also been scaled back. Taxpayers can claim a deduction of no more than $10,000 for the sum of state and local property taxes and either income or sales taxes.

In the past, homeowners could deduct the interest from a HELOC (Home equity line of credit) or home equity loan for non-property related expenses. Now, only interest on loans used to purchase, build or substantially renovate your home is eligible. The section on home equity is complex and open to interpretation. Cosmetic updates may not meet the IRS’s definition of “substantial.”

One above-the-line deduction, which means you can take even if you don’t itemize, for moving expenses has been suspended for 2018-2025.

The National Association of Realtors worked to preserve the tax benefits of homeownership during the writing of the bill. Unfortunately, for both families and single buyers, the new law is taking away some of the tax incentives of owning a home instead of renting.