Exceeding customer expectations is a well-cited core value of many companies, but it’s often easier said than done, especially when trying to clear the title on a property with a 32-year-old mortgage from a defunct lender with a missing mortgage assignment and satisfaction.

Every settlement agent knows the frustration of solving a mystery of missing satisfactions, releases, assignments, and other documents necessary to clear a cloud on a title and sell a property without resorting to quiet title. Like Hansel and Gretel leaving bread crumbs along the forest path, a missing document in the property’s paper trail can lead to a nightmare.

When we received first contact with Barbara from Magnolia Abstract Services, Inc. about this Title Curative case, we found her in a forest of email correspondence with a competitor who had been working on solving a title curative case for six months with no resolution in sight. She reached out to us to see if we could potentially help her cause.

The mystery of the missing mortgage assignment and satisfaction

A mortgage assignment is a document showing a mortgage has been transferred from the original lender or borrower to a third-party. A mortgage satisfaction is a document indicating that the loan has been paid in full. A homeowner will also receive a “paid in full” letter from their lender, which is needed to record the satisfaction, but is not the same document. Both the assignment and satisfaction are shown in the public record and will be found in a title search. A clean title will have no break in the chain of title or missing “bread crumbs” in the paper trail of assignments from one lender to another.

In this case, the mortgage loan was originated in 1986 and completely paid off in 1999. The mortgage had been transferred three times, meaning a total of four lenders held an interest in the property at some point. The current owners had no mortgage satisfaction recorded; however, they had received a paid in full letter from the last lender of record, Atlantic Mortgage.

In addition to a missing mortgage satisfaction, there was also a missing mortgage assignment from the first lender, The Greater New York Savings Bank, to the second. Because there was no assignment from the first to second lender and the last lender of record, Atlantic Mortgage, had been merged and acquired by several entities since the paid in full letter had been sent, the current lender responsible for recording the satisfaction, CitiMortgage, refused to do the recording until the missing assignment was found and recorded.

The competition’s response

Our client had been working with a Senior Title Curative Specialist at another title curative company for nearly six months. She received an email with a status update informing her that CitiMortgage was waiting on Astoria Financial as the successor to The Greater New York Savings Bank to file the assignment. Unsatisfied with the delay, she requested contact information for a manager at Astoria to expedite the process, but the Curative Specialist didn’t have that information.

Two weeks later, the client reached out again with documents alerting the Curative Specialist that Astoria was now merged with Sterling Bancorp. In response, the Curative Specialist advised that the documents wouldn’t help in obtaining the missing assignment as the original lender was no longer in business and Astoria, now Sterling, has no record of the original loan due to its age. The Specialist explained they had reached out to Prudential Financial (successor to the second lender) to see if they had any records that may help Astoria produce the assignment and complete the chain of title so that CitiMortgage may proceed with the release of the mortgage.

However, it was highly unlikely that Prudential would be able to assist since the assignment was recorded by another entity decades ago. The Curative Specialist ended the email by advising the client to consider resolving the matter through a quiet title with a real estate attorney.

The suggestion to resort to quiet title indicated that the competition was ready to wring their hands of the problem file. That’s when our client decided to take another approach and reached out to us.

Solving the case

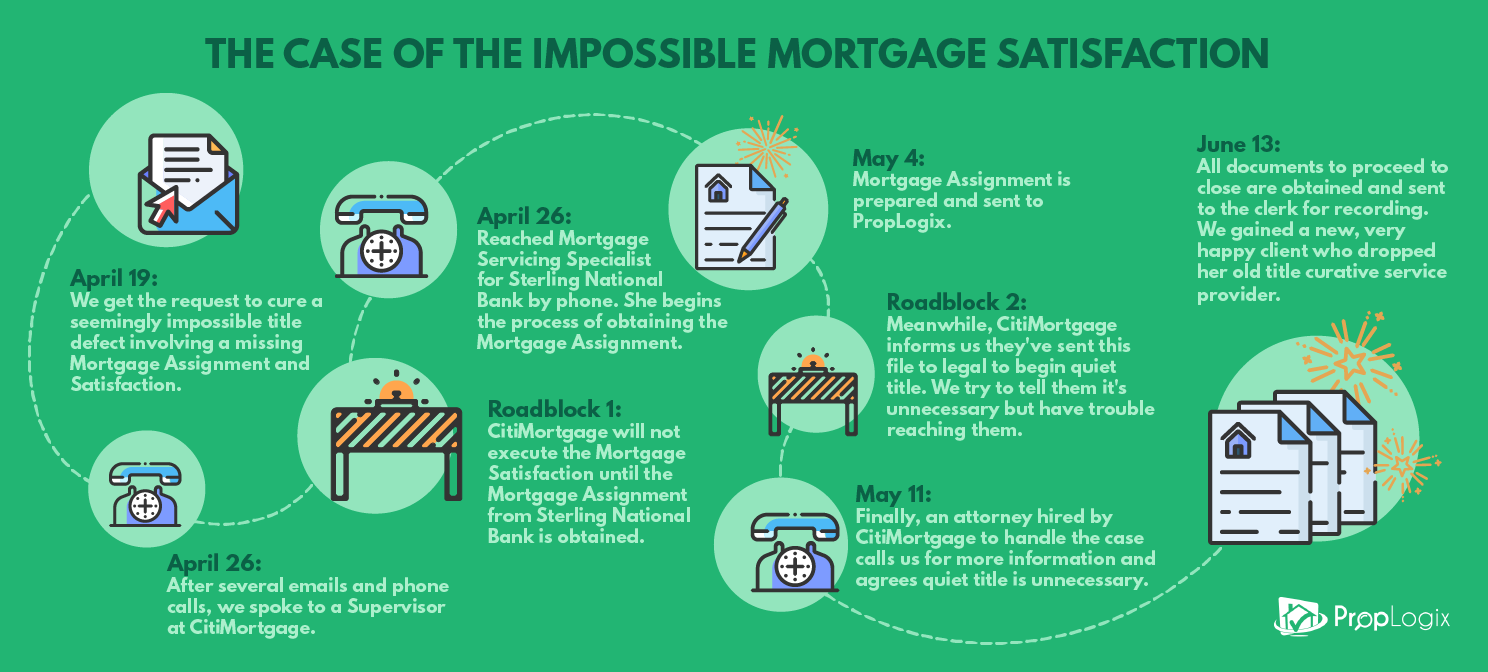

Our Release Tracking Specialist, Adam, received an email with the title report and paid in full letter addressed to the current owner and seller. After doing some digging, he began contacting the lenders involved. First, he reached out to a supervisor in the lien release department at CitiMortgage to get an update on what documents they required to execute and record the satisfaction. They confirmed that they were waiting on the first lender to produce the assignment.

Next, he spoke to a Supervisor at Sterling, who by happenstance was also working for the company when it was Greater Savings Bank. She was confident that they could produce the assignment based on their records, so she requested that Adam fax her all the documents related to the file, including the paid in full letter.

One week later after sending the documents, the Supervisor at Sterling had prepared and sent the assignment to us via mail. Ecstatic about the quick response from Sterling, Adam called the client to tell her the good news and discuss the next steps. Typically, for a Release Tracking file, a client is given the option to let our Release Tracking Specialists record the documents on their behalf and add the county recorder fees on the final invoice or send them the documents to record. However, the client advised that since recording fees in Suffolk County cost $600 dollars, we should first contact CitiMortgage and confirm they will record the satisfaction before spending money to record the assignment.

Can’t get no satisfaction

The thrill of finally receiving the assignment from Sterling was quickly thwarted when speaking to the customer representatives at CitiMortgage. They told Adam that they were no longer handling this file, and that it was sent to their legal department to file quiet title because there was no assignment. Adam explained that he had the assignment, so performing quiet title would be unnecessary and expensive at this point. He requested to speak to someone in the lien release or legal department who was handling the file.

The first time calling, he was sent to a voicemail. The second time, he was informed by the customer representative that they don’t take inbound calls. After making several calls and leaving several voicemails searching for the individual in charge of this file, the customer service representative stated again that the legal department didn’t take inbound calls and asked him to please stop calling.

Persistence pays off

Finally, after speaking to multiple supervisors and representatives, Adam received a call from an attorney that had been hired by CitiMortgage looking to be filled in on this file that had just hit his desk. The attorney agreed that quiet title would be unnecessary with the mortgage assignment in hand. He confirmed with the county recorder that both documents could be simultaneously recorded. Due to the lengthy time it would take to officially record all the documents, an undertaking letter would accompany the copies of the satisfaction and assignment assuring that both documents would be recorded by the attorney in order to help expedite our client’s closing.

After a few weeks of waiting, the CitiMortgage finally approved the satisfaction. The attorney sent the original assignment and satisfaction to the county to be recorded, and with the undertaking letter and copies of the assignment and satisfaction our client was able to proceed with the closing. After roughly two months of working and pushing to get these documents obtained and recorded, Adam and our client, Barbara, were elated to finally have the file resolved.

“That’s why I like this… it’s just problem solving. You just have to figure out what you have to do to get it done. I want to put in the effort that I would see if it was my file,” Adam explains.

Not everyone is as helpful as the supervisor at Sterling or the attorney hired by CitiMortgage. A part of problem solving in Title Curative cases is understanding how to work with the people you have to rely on to complete the task at hand from the customer service representatives to the municipality workers to the attorneys executing documents. Through a combination of persistence, persuasion and a little luck, our Release Tracking Specialist was able to resolve a file in about two months that our competitors worked on for over six months. Taking just a few extra steps, making a few extra calls, and spending a little more time to persuade those on the other end of the line to champion our cause made the impossible mortgage satisfaction possible.