Predictions in the real estate industry can be tricky. While concerns over an approaching housing bubble are boiling over for some people, without a crystal ball, we’d be remiss to make any claims as to when another recession might be… if at all.

However, there are some demographic trends among homebuyers, and technological advancements paired with legislative changes, that will forever change the real estate transaction experience. Here are some of the trends the real estate and title industry are seeing and what professionals should know when working with clients.

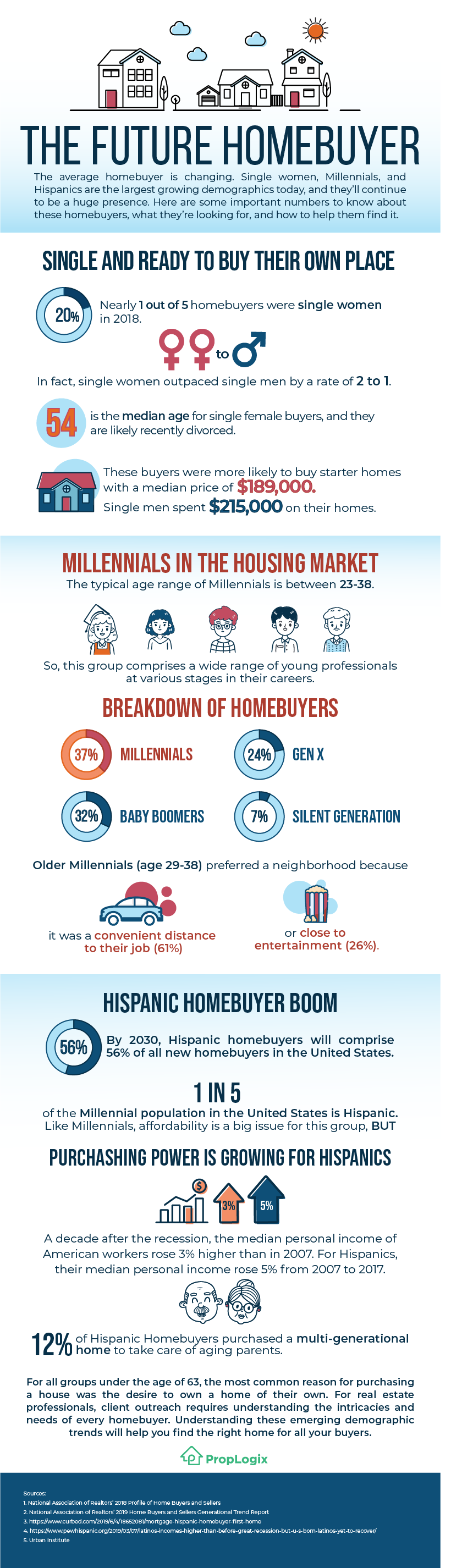

Changing demographics of homebuyers

By now, you’ve probably heard about the changing face of the average homebuyer. Single women, Millennials, and Hispanics are more likely to be buying homes today. For real estate professionals, it’s important to understand who these buyers are, what their wants and needs are, and how to appeal to them.

Single and ready to find a place of their own

In 2018, approximately a fifth, or 18%, of homebuyers were single women, according to the National Association of Realtors’ 2018 Profile of Home Buyers and Sellers. Making them the second-largest homebuying group behind married couples, and they are outpacing single men by a rate of nearly 2 to 1. Some reasons for the surge among this group is due to relationship changes, a tendency to prefer entry-level and starter homes, and a desire to carve out a space of their own.

The median age for single female buyers is 54 years old, and many are likely coming out of a divorce. A significant portion (39%) of these buyers reported using proceeds from the sale of a previous primary residence. As a result, they are less likely to dip into their savings accounts to cover the down payment and closing costs than single men and married couples. They are also more willing to purchase a starter home. According to data from the NAR, the median home price for single women was $189,000 compared to $215,000 for single men.

From the numbers, it’s clear that these single women are willing to sacrifice space and purchase a humble abode in order to avoid overextending their finances. What matters most is finding a place they can make their own and suits the needs of their family.

Millennials continue to enter the homebuyer market

The typical age range of the demographic known as Millennials is between 23-38. The median first-time homebuyer in the U.S. is 34 years old, which means this group is quickly becoming the biggest group of homebuyers.

There are a lot of financial barriers for the group to overcome in order to realize their dream of homeownership. According to a Zillow analysis, buyers today need to save 1.5 years longer for a down payment than they did 30 years ago. This is due in part to student loan debt and a decrease in purchasing power for the average paycheck. Securing a loan is also more difficult. About 29% of first-time homebuyers were denied a mortgage at least once.

In addition to the struggle to save money and secure a loan, many homebuyers in this age range are reporting buyer’s remorse. The number one contributing factor was the hidden costs associated with buying and owning a home. Closing costs, property taxes, homeowners insurance, private mortgage insurance (for those who don’t put down at least 20%), and upkeep are a part of the real estate transaction and the reality of homeownership. Location was another aspect playing a role in their regret. This may be in part to Millennials being more apt to make an offer on a home sight unseen.

When working with a first-time Millenial homebuyer, agents should be ready to educate them on the closing costs associated with the transaction and encourage the buyers to take the time to see the home in-person. Suggest visiting the neighborhood at different times during the day to get an idea of the daily rhythms of activity.

Hispanic homebuyer boom

According to the Urban Institute, Hispanic homebuyers will comprise 56% of all new homebuyers in the United States by 2030. It’s important to remember that this demographic comprises a large collection of people from various nations, the common denominator being that individuals are from a Spanish speaking nation. The Hispanic population is itself diverse, but some studies have shown that there are still some similarities within this varied group. As a whole, there is a cultural and financial emphasis placed on the value of homeownership.

Hispanic first-time homebuyers face many of the same barriers that Millennials do: affordability and financing. Data from 2015 shows that a little over 19% of Hispanic mortgage applicants were rejected for a loan. Despite these obstacles, the buying power of this demographic is expected to increase. Over the past decade, the median income of Hispanic households grew from $43,566 to $50,486. There is also a lot of overlap between the two demographics. Nearly a fifth of the Millennial population in the United States is Hispanic.

Like Millennials, there is also a need to help this group better understand their financing options in order to avoid loan products with burdensome fees and down payments. According to the National Association of Hispanic Real Estate Professionals, 57.2% of Hispanics opted for conventional financing while 79.4% of non-Hispanic homebuyers chose conventional loan packages.

In order to accommodate and appeal to this group of homebuyers, real estate professionals will want to spend time understanding the intricacies and overlap with other demographics. For example, Hispanic Millennials are closer to their families and are looking for places suitable for their mom and dad to live with them. Agent outreach to this group will require strategy and hyper-segmentation. Brushing up on your Spanish isn’t enough.

The changing technology in the title industry

The average homebuyer demographic isn’t the only big change happening at the closing table. How we apply for mortgage loans, how real estate agents interact with their clients, and how title agents coordinate and execute the settlement are being affected, for good or bad, by changing technology.

It may seem overwhelming and concerning for those in real estate who have been used to doing things a particular way for years. This sentiment was reflected in some of the responses we received from our latest State of the Title Industry survey.

One of the respondents of the survey voiced worry over changes happening too quickly, “This business has gotten too automated. We need to slow down and continue doing our jobs correctly ourselves, individually, to protect consumers.”

Another respondent, however, exclaimed, “Everything is paper! I’m used to scanned files. Working this way is so archaic.”

While the title and real estate industry is moving to a more streamlined experience for the homebuyer, the truth is, compared to other industries, there is still an overwhelming amount of paper and friction points between the professionals communicating to close a deal. Remote Online Notarization and other advances in machine learning are helping to reduce the overall friction and make the process easier and less error-prone for professionals and consumers.

How many digital closings have been completed so far?

Since 2017, The Mortgage Bankers Association has teamed up with the American Land Title Association to ensure state RON laws are consistent with MISMO standards. The campaign has been successful in introducing over 30 RON bills based on the MBA-ALTA model, and Remote Online Notarization legislation aligned with these standards has been enacted in 22 states so far. These standards are important for title agents and agent-attorneys as it will make the implementation of remote notarization consistent and execution of future closings easier across the country. Settlement agents are encouraged to get involved with their state land title associations to help with the initiative.

There hasn’t been a straight forward adoption of digital closings across the United States. There’s also a bit of a nebulous definition of what constitutes a digital or eClosing. While RON laws mean that a fully digital closing from mortgage origination to settlement is possible in more and more states, many title insurance underwriters, lenders, and title companies have opted for a hybrid eClosing solution where some documents are eSigned but other documents require a wet signature.

As a result, it’s difficult to ascertain an exact number of how many have been completed. However, First American Title, one of the “big four” in the title industry, has completed 500 hybrid eClosings. Another one of the big four, Stewart, completed their first 100% paperless, fully-digital transaction in Texas back in July of 2018 and has conducted hundreds of RON closings since then.

The numbers of digital closings are steadily rising around the world, so the next time you close on a property, you might be signing the papers in your pajamas or while you’re on vacation in Maui.